+ The sharp recovery from the pandemic in conjunction with the considerably positive developments in tourist traffic and the relevant proceeds during the summer period, created optimism regarding the performance of the sector and the Greek economy in general.

– However, the deterioration of the international economic climate with the ongoing geopolitical instability and energy crisis, led to an increase in costs and prices in general, preserving a climate of uncertainty.

– Huge increase in the price of fuels that formed in unprecedented levels, burdened excessively the operating cost, absorbed the benefit from turnover increase, worsened significantly the operating results and prevented the effort to preserve adequate working capital.

Statistics

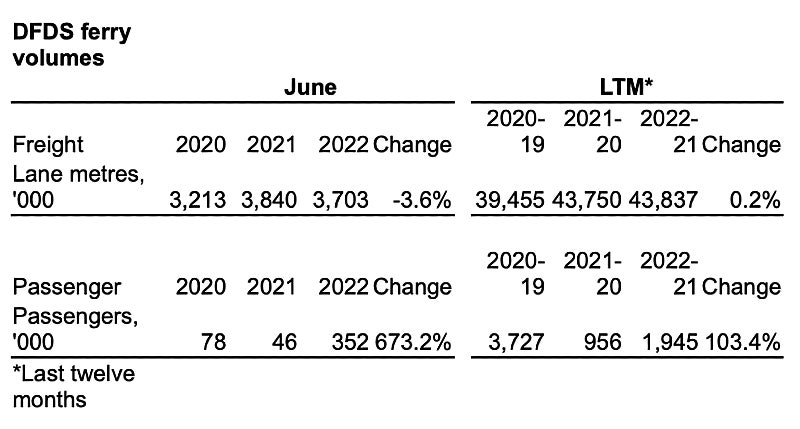

-15% itineraries / +61% pax / +28% vehicles / -11% freight units

Financial figures

+28% Group Turnover EUR 74.2 million

+13% Parent company turnover EUR 64.7 million

EBITDA

Group losses of EUR 12.0 million over EUR 0.7 million

Parent Company losses of EUR 11.7 million versus EUR 1.6 million.

Financial Results

The net financial cost of the Group and the Parent Company amounted to EUR 5.6 million versus EUR 5.4 million.

Net Results

Consolidated net results after taxes and minority interests for the first half of 2022 amounted to losses of EUR 22.6 million over EUR 12.1, while correspondingly, Parent Company’s net results after taxes formed at losses of EUR 20.7 million versus EUR 11.9 million.

ANEK > Attica

On 26 September 2022, the Company’s Board of Directors decided –following the agreement between Attica and the major creditors and shareholders of ANEK– the commencement of the procedure